US Manufacturing Hits Four-Year High as Nvidia Lifts Wall Street to Records, But Iran Talks Collapse Spikes Oil 6% and European Tariffs Signal a Deeply Divided Global Economy in June 2026

Tuesday, June 2, 2026 | Breaking News

The global economy sent contradictory signals on Tuesday, June 2, 2026, presenting investors, policymakers, and businesses with a picture of genuine strength in certain corners of the American economy colliding with the most severe geopolitical supply shocks in decades. US equity indices closed at record highs Monday, driven by Nvidia’s PC chip announcement and a stronger-than-expected ISM Manufacturing print that hit a four-year high, suggesting American industrial output is accelerating despite the tariff war and oil shock. Yet oil prices spiked 6 percent after Iran suspended peace talks with the United States and threatened to close the Strait of Hormuz and the Bab el-Mandeb, two waterways through which roughly 30 percent of the world’s seaborne energy trade flows. The dual signal, Wall Street records alongside oil-driven inflation risk, defines the impossible tension at the heart of the global economy in 2026.

The ISM Manufacturing Index reaching a four-year high is the single most encouraging domestic economic data point in months. The headline reading of 54.0 was driven by new orders jumping 2.7 points to 56.8, suggesting AI-related capital expenditure and infrastructure spending continue to flow through the US industrial base at an accelerating pace. Employment in manufacturing improved to 48.6, though it remained technically in contraction territory. Prices paid eased to 82.1 but stayed sharply elevated, reflecting the persistent cost of tariffs on imported inputs and the oil price shock flowing through logistics networks. The Atlanta Federal Reserve’s GDPNow model cut its second-quarter GDP estimate to 3.0 percent from 3.8 percent, complicating the interpretation of an otherwise strong manufacturing headline.

Nvidia drove the market higher with the most consequential product announcement in the technology industry so far this year. The RTX Spark Superchip, unveiled at Computex 2026 in Taipei, enters Nvidia into the $200 billion PC processor market for the first time, pitting the world’s most valuable company against Intel, AMD, and Qualcomm on their traditional home turf. Wall Street’s reaction reflected both the genuine strategic significance of the move and the extraordinary confidence investors have placed in CEO Jensen Huang’s ability to execute on ambitious roadmaps. Nvidia fiscal year 2026 revenue already reached a record-breaking $215.94 billion, a 65 percent year-over-year increase, and the RTX Spark announcement opens an entirely new revenue stream. Cathie Wood’s Ark Investment Management purchased 300,000 Nvidia shares following the PC chip launch.

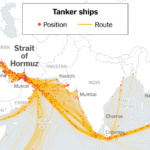

The oil spike immediately complicated the positive market picture. Brent crude jumped more than 5 percent on Monday after Iran’s Tasnim News Agency reported that Tehran was suspending peace negotiations with Washington over Israel’s Lebanon strikes and that the Islamic Republic is determined to consider closing both the Strait of Hormuz and the Bab el-Mandeb Strait. The simultaneous threat to two major global energy chokepoints is without modern precedent. A dual closure would remove the alternative routing that tankers had adopted after the initial Hormuz disruption, leaving no viable shortcut between Persian Gulf oil production and European or Asian consumers. Analysts at multiple investment banks issued emergency research notes warning that Brent could reach $130 per barrel or higher within days if Iran follows through on the Bab el-Mandeb threat.

European markets bore an additional burden as the 25 percent US tariffs on goods from Germany, France, the United Kingdom, the Netherlands, Sweden, Denmark, Norway, and Finland took full effect on June 1. The Frankfurt DAX and Paris CAC indices both fell on Monday as German auto stocks led the decline, with BMW, Mercedes-Benz, and Volkswagen each retreating sharply on concerns that 25 percent tariffs on top of the earlier automotive-specific levies make European vehicles economically uncompetitive for American buyers. The euro weakened against the dollar, providing some export relief for European goods sold in non-US markets but also importing inflation through higher energy costs denominated in dollars.

The ITIF published its one-year assessment of how countries are adapting to the so-called ‘Liberation Day’ tariffs that reshaped global trade beginning in April 2025. The report, published June 1, 2026 by representatives from 30 economies across 25 countries, finds that while some bilateral negotiations produced narrow deals, the dominant global response has been supply chain diversification, new regional trade agreements, and a permanent reduction in confidence in the US market as a stable destination for long-term export strategy. Countries across Southeast Asia, Latin America, and Africa accelerated plans to deepen trade relationships with China, the European Union, and regional partners rather than rebuilding dependence on American market access subject to sudden tariff shocks.

Read More: Global AI Industry Revolution: Colorado’s Historic AI Law Activates June 30 as US-EU Regulatory Race Accelerates and Tech Giants Face Billion-Dollar Compliance Costs

For the Federal Reserve, the June 2 economic picture represents a nearly impossible policy environment. Manufacturing strength and record equity prices might ordinarily encourage a reduction in interest rates to sustain momentum. But oil prices rising toward $100 per barrel, tariff-driven goods inflation persisting well above target, and the persistent risk that Iran’s Hormuz and Bab el-Mandeb threats materialize into actual closures argue strongly for maintaining tight monetary policy to anchor inflation expectations. Fed Chair Jerome Powell, speaking in Washington last week, acknowledged that the dual supply shocks from tariffs and the oil war create conditions where the standard tools of monetary policy are ‘substantially constrained in their effectiveness,’ a remarkably candid admission that central banks cannot easily resolve shocks originating from geopolitics.

The week ahead tests every assumption markets made entering June. If Iran follows through on the Bab el-Mandeb threat, oil prices break higher with immediate consequences for global growth projections. If Trump succeeds in pressuring Israel to pause Lebanon strikes and Iran returns to negotiations, oil prices could drop sharply toward $80 per barrel, providing unexpected relief to inflation-stressed economies worldwide. If the European Union activates its retaliatory tariff package against US exports, the transatlantic trade war enters a new escalatory phase. And if Nvidia’s RTX Spark confirms the new direction of AI computing, the technology sector may continue to decouple from the broader economic anxiety, sustaining stock market optimism even as physical economy conditions deteriorate. In 2026, the gap between financial markets and economic reality has rarely been wider or more consequential.